“Telleroo is a game changer for accountants. No more banking access and Bacs SUN numbers needed. We highly recommend it to our clients that value efficiency and reliability!”

Right first time: Why strong AML processes are key to growing your firm

Words by

Charlotte Russell

May 11, 2026

May 11, 2026

Growth and compliance often get treated as separate goals in accounting firms, and they shouldn't be! When your anti-money laundering processes are strong, consistent, and built into how your firm works, they do more than help you meet regulatory duties. They save time, reduce risk, improve client onboarding, and create a better foundation for growth.

This matters for UK accounting firms facing rising expectations around client due diligence, risk assessments, and identity verification. It also matters for practice leaders who want to scale without creating extra admin or exposing the firm to avoidable gaps. The firms that get Anti-Money Laundering (AML) right early are often the firms that run more efficiently later.

In this article, we look at why AML shouldn't be treated as a tick-box exercise, what strong AML processes look like in practice, how the regulatory landscape is changing, and how better onboarding can support both compliance and commercial growth.

Why strong AML processes support firm growth

It is easy to think of AML as a compliance cost. In reality, poor AML is often what creates the bigger cost.

When firms cut corners at onboarding or collect incomplete information, the same work comes back later. Teams have to chase documents again, repeat checks, revisit risk decisions, and fix gaps under time pressure. That creates friction for staff and clients alike.

Strong AML processes help firms grow because they:

Reduce rework and duplicated admin

Create a smoother client onboarding experience

Support consistent decisions across the team

Lower the risk of missed compliance obligations

Give firms better-quality client information from the start

The key takeaway is simple: good AML is not separate from operational efficiency. It is part of it.

Why AML should not be a tick-box exercise

A common problem in firms is that AML gets treated as something to complete, file, and forget. That mindset limits its value.

If AML is only a form-filling task, it becomes disconnected from the wider client relationship. Teams gather the minimum needed to move forward, rather than using the process to understand who the client is, how their business works, and where potential risks or opportunities sit.

What goes wrong with a tick-box approach

A narrow approach often leads to:

Incomplete client information

Inconsistent onboarding standards

Missed risk indicators

Duplicated checks later in the client lifecycle

Fewer meaningful conversations with clients

This can also weaken commercial performance. If your team does not ask the right questions at the start, they may miss signs that a client needs extra support with bookkeeping, payroll, payments, company secretarial work, or advisory services.

A better way to think about AML

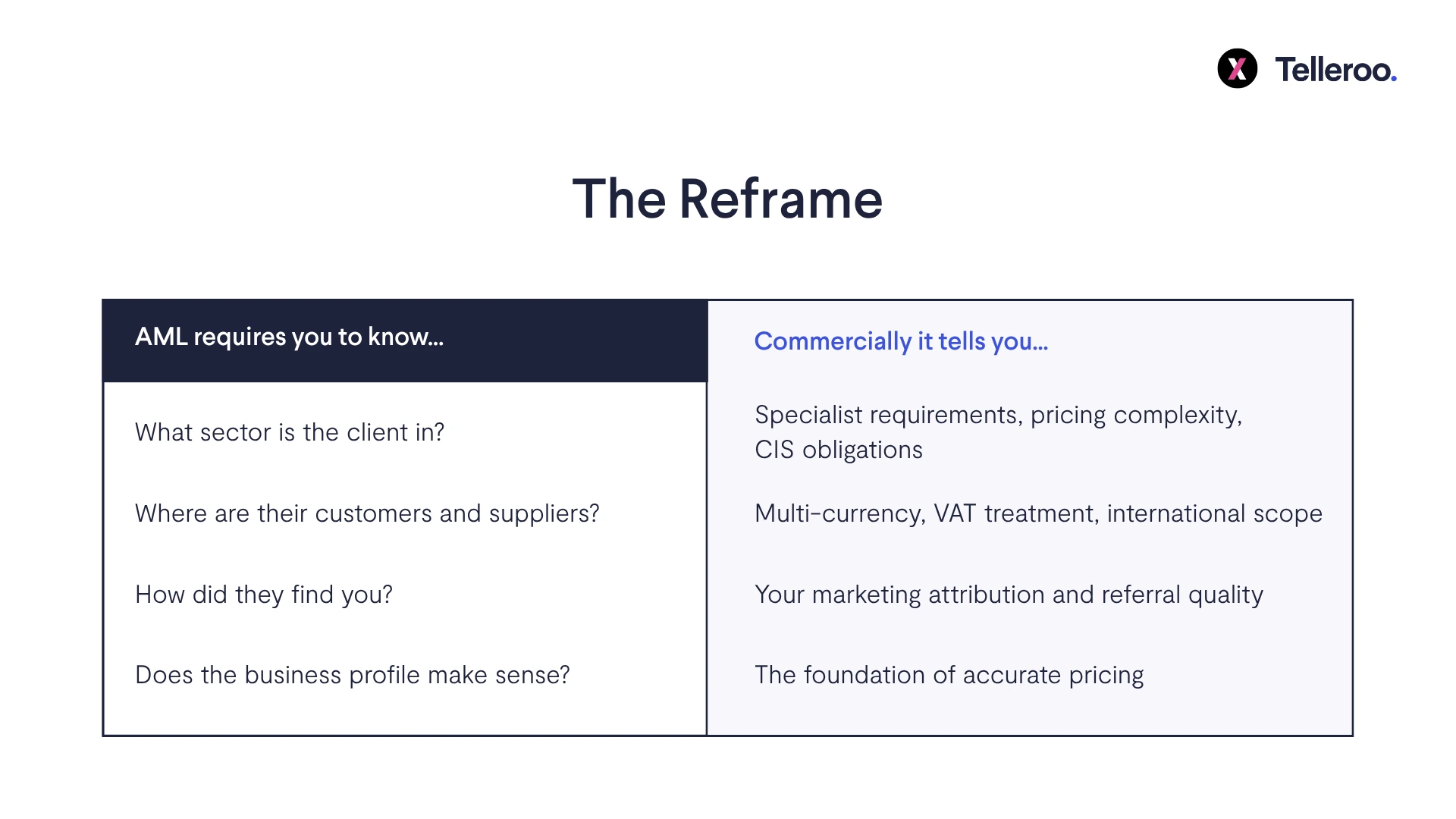

Strong AML should be built into the client journey, not bolted onto it. That means using onboarding and due diligence as a structured way to understand the client, assess risk properly, and gather information that will be useful beyond compliance alone.

For example, a client due diligence conversation can help you confirm ownership and control, understand the nature of the business, and identify how the client expects to work with your firm. That makes your compliance stronger, but it also gives your team better context for service delivery.

Takeaway: AML works best when it is treated as part of good practice management, not just a regulatory task.

What strong AML processes look like in practice

Good AML is not about making things more complex. It is about doing the right work at the right time, in a way that supports consistency.

Three core elements matter most: client due diligence, risk assessments, and onboarding.

Client due diligence: get the right information early

The best time to collect key information is at the start of the client relationship. If you miss it then, you often pay for it later.

Client due diligence should give your firm a clear view of:

Who the client is

Who owns or controls the business

What the business does

Whether there are any higher-risk factors

What documents and evidence support your assessment

Why timing matters

Capturing relevant information early helps firms avoid delays, repeat requests, and re-verification later. It also makes it easier to onboard clients smoothly when other checks or services rely on the same core data.

For example, if your initial identity checks do not meet the standard required for another process down the line, your team may have to go back to the client and start again. That costs time, adds friction, and can undermine the client experience.

Best practice for due diligence

To make due diligence more effective:

Collect complete information at the start, not in stages unless necessary

Use a standard process across the firm

Make sure evidence is easy to retrieve later

Align data capture with likely future compliance needs

Avoid accepting the bare minimum if stronger evidence is easy to obtain now

Takeaway: the more complete your onboarding data is at the start, the less duplication your team will face later.

Risk assessments: a live process, not a one-off task

Risk assessments are only useful if they reflect the client’s actual position. That means they cannot sit untouched for years.

A practical approach is to review risk assessments regularly and tie them to work your firm is already doing.

When to review risk assessments

For many firms, a sensible rhythm is to review client risk assessments:

Annually

Alongside year-end work

When completing SA100s

When there is a material change in ownership, activity, or risk profile

This makes the process easier to manage because it fits into existing workflows. It also reduces the chance that changes go unnoticed.

Why regular reviews matter

A client who looked low risk at onboarding may not look the same a year later. Their business model may change. New owners may come in. Their filing behaviour may shift. Their transaction patterns may raise new questions.

By reviewing risk assessments regularly, firms can:

Keep records accurate

Respond to changes sooner

Support better decision-making

Show a clearer compliance trail

Takeaway: risk assessments should move with the client relationship, not remain frozen at the point of onboarding.

The changing regulatory landscape raises the standard

AML processes do not exist in isolation. Firms also need to respond to wider regulatory change, including identity verification requirements linked to Companies House.

This is where many firms can run into avoidable inefficiency.

What firms need to know about Companies House identity verification

Directors and people with significant control, often called PSCs, must meet identity verification requirements at Companies House. That means firms need to think carefully about whether the information they collect during onboarding will also support these needs.

If it does not, firms may find that AML checks completed earlier are not enough for later verification requirements. The result is more chasing, more admin, and more cost.

The risk of not aligning processes

If firms gather only what is needed for one narrow AML task, they may later discover that the information does not satisfy Companies House expectations. Then they need to reverify the same person.

That duplication creates problems:

Staff spend time repeating work

Clients are asked for information twice

Onboarding feels fragmented

Compliance costs rise unnecessarily

Why alignment matters

A smarter approach is to align identity verification with AML processes from the start where possible. This helps firms build a stronger and more reusable compliance record.

That does not just reduce admin. It also helps your team work with more confidence because they know the initial process was designed with future requirements in mind.

Takeaway: aligning AML and identity verification early can save firms from expensive rework later.

How better onboarding improves efficiency and client experience

Onboarding is often where compliance and commercial performance meet most clearly. If the process is unclear, slow, or repetitive, both the client and your internal team feel it.

A strong onboarding process should achieve three things at once:

Meet AML obligations properly

Collect information that supports future work

Create a smooth first experience for the client

What good onboarding looks like

Good onboarding is structured, consistent, and easy to follow. It asks for the right information once, explains why it is needed, and stores it so the team can use it again when required.

For example, if your firm aligns onboarding with AML and identity verification requirements, you are less likely to revisit the same documents later for another compliance step or service setup.

Using AML conversations to surface client needs

This is an area many firms overlook. The questions asked during AML and onboarding can reveal useful business context.

You may learn that:

The client has plans to grow quickly

Ownership structures are changing

There are gaps in financial processes

The business needs support with payments or controls

There may be future advisory opportunities

That does not mean turning compliance into a sales pitch. It means listening carefully and using the conversation to understand the client better.

Takeaway: strong onboarding does more than reduce risk. It also gives your firm a stronger starting point for service delivery and growth.

Practical AML best practices for UK accounting firms

If you want to improve AML without making it heavier than it needs to be, focus on a few practical habits.

Do

Capture relevant client information at the start of the relationship

Align ID verification with AML processes where possible

Review and update client risk assessments regularly

Build AML into existing workflows such as year-end reviews

Use due diligence conversations to better understand the client’s business

Keep records consistent and easy to access

Do not

Treat AML as a one-off admin task

Rely on incomplete onboarding to save time

Assume old risk assessments still reflect the current position

Separate compliance conversations from the wider client context

Wait until a later regulatory need forces you to reverify information

Takeaway: small process improvements at the start usually prevent much bigger problems later.

Using Xama with Telleroo: a simpler way to share KYC documents

When firms already hold client due diligence information in Xama, sharing that information during Telleroo onboarding can be much simpler.

The using Xama and Telleroo together allows users to share KYC documents directly instead of downloading and re-uploading them manually. That helps reduce admin and makes onboarding more efficient.

Log into Xama and open the client you want to invite to Telleroo.

Click Telleroo Share.

Copy the one-time code shown in the pop-up.

Log into Telleroo and click Invite Client.

Complete the usual client details.

In the AML compliance checks section, tick Use a Xama code.

Paste the code into the box provided.

Save and continue with the normal Telleroo invite process.

Once the invite is submitted, Xama shares the client’s KYC documents with Telleroo directly.

Why this matters for firms

This integration helps firms:

Reduce manual handling of documents

Avoid unnecessary download and re-upload steps

Speed up onboarding

Make better use of information already collected during AML checks

For firms focused on efficient, compliant onboarding, that kind of workflow matters. It removes friction from a process that can otherwise become repetitive.

Takeaway: Using Xama and Telleroo can make client payments onboarding faster and easier by reusing verified KYC information.

Strong AML processes help accounting firms do more than meet compliance obligations. They improve onboarding, reduce duplication, support better risk management, and give firms stronger foundations for growth. When you collect the right information early, review risk regularly, and align AML with wider verification requirements, you create a process that is both safer and more efficient.

The biggest shift is mindset. AML should not sit in a silo as a tick-box task. It should be part of how your firm understands clients, manages risk, and runs well at scale. If you want to improve results, start by reviewing your onboarding process and identifying where stronger AML could remove friction later.

FAQs

Q: Why is AML important for accounting firm growth? A: Strong AML processes reduce rework, improve onboarding, support compliance, and give firms better-quality client information. That helps firms scale more efficiently.

Q: How often should client risk assessments be reviewed? A: A practical approach is to review them annually and alongside key work such as year-end accounts or SA100 completion, as well as after major client changes.

Q: Why should firms align AML with Companies House identity verification? A: Alignment helps avoid duplication and re-verification later, especially for directors and PSCs who must meet identity verification requirements.

Q: How does the Xama and Telleroo integration help? A: It allows firms to share KYC documents directly from Xama into Telleroo using a one-time code, reducing manual document handling during onboarding.

.png)

QuickBooks BillsPay QuickBooks invoices in a few clicks.

QuickBooks BillsPay QuickBooks invoices in a few clicks. ExpenseInPay approved expenses from ExpenseIn.

ExpenseInPay approved expenses from ExpenseIn. Employment HeroSync payroll from Employment Hero.

Employment HeroSync payroll from Employment Hero. FreshPaySync pay runs from FreshPay.

FreshPaySync pay runs from FreshPay. StaffologyImport payroll from Staffology.

StaffologyImport payroll from Staffology. SafeHRSync payroll from SafeHR.

SafeHRSync payroll from SafeHR..png) BuddyConnect Buddy HR payroll.

BuddyConnect Buddy HR payroll. PaiyrollConnect Paiyroll to Telleroo.View all integrationsBrowse the full directory.

PaiyrollConnect Paiyroll to Telleroo.View all integrationsBrowse the full directory.

.webp)

.webp)

'%3e%3cg id='Final-Copy-2_2_' transform='translate(1275.000000, 200.000000)'%3e%3cpath class='st0' d='M7.4,12.8h6.8l3.1-11.6H7.4C4.2,1.2,1.6,3.8,1.6,7S4.2,12.8,7.4,12.8z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3cg id='final---dec.11-2020'%3e%3cg id='_x30_208-our-toggle' transform='translate(-1275.000000, -200.000000)'%3e%3cg id='Final-Copy-2' transform='translate(1275.000000, 200.000000)'%3e%3cpath class='st1' d='M22.6,0H7.4c-3.9,0-7,3.1-7,7s3.1,7,7,7h15.2c3.9,0,7-3.1,7-7S26.4,0,22.6,0z M1.6,7c0-3.2,2.6-5.8,5.8-5.8 h9.9l-3.1,11.6H7.4C4.2,12.8,1.6,10.2,1.6,7z'/%3e%3cpath id='x' class='st2' d='M24.6,4c0.2,0.2,0.2,0.6,0,0.8l0,0L22.5,7l2.2,2.2c0.2,0.2,0.2,0.6,0,0.8c-0.2,0.2-0.6,0.2-0.8,0 l0,0l-2.2-2.2L19.5,10c-0.2,0.2-0.6,0.2-0.8,0c-0.2-0.2-0.2-0.6,0-0.8l0,0L20.8,7l-2.2-2.2c-0.2-0.2-0.2-0.6,0-0.8 c0.2-0.2,0.6-0.2,0.8,0l0,0l2.2,2.2L23.8,4C24,3.8,24.4,3.8,24.6,4z'/%3e%3cpath id='y' class='st3' d='M12.7,4.1c0.2,0.2,0.3,0.6,0.1,0.8l0,0L8.6,9.8C8.5,9.9,8.4,10,8.3,10c-0.2,0.1-0.5,0.1-0.7-0.1l0,0 L5.4,7.7c-0.2-0.2-0.2-0.6,0-0.8c0.2-0.2,0.6-0.2,0.8,0l0,0L8,8.6l3.8-4.5C12,3.9,12.4,3.9,12.7,4.1z'/%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/g%3e%3c/svg%3e) Manage Cookies

Manage Cookies